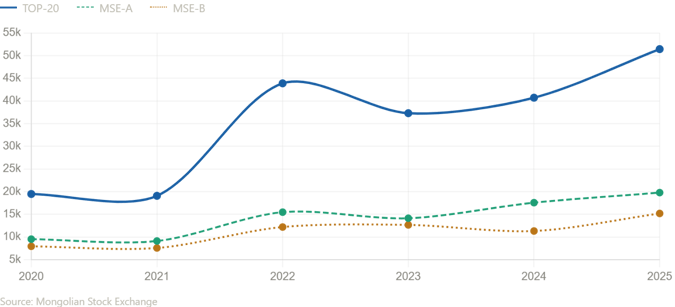

A market that has returned 164% in five years should not be invisible to global allocators. The Mongolian Stock Exchange TOP-20 index closed 2025 at 51,455 points, up from 19,491 in 2020, yet Mongolia remains a market most investors have never opened a terminal to examine.

That neglect is the opportunity. Mongolia in 2026 offers multiple investment channels that deserve more analytical attention than they currently receive.

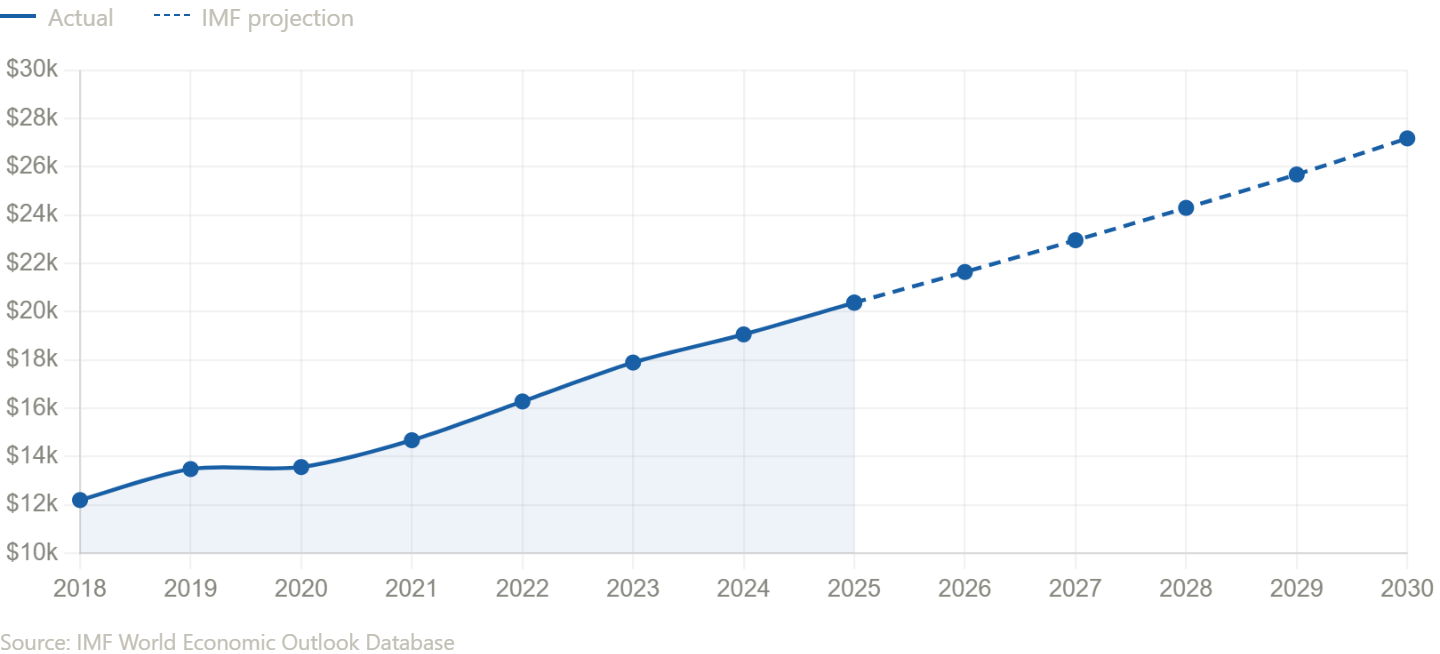

GDP per capita in purchasing power parity terms has risen from US$12,202 in 2018 to US$20,378 in 2025, according to IMF data. The IMF projects this to reach US$27,184 by 2030. That trajectory has held across a commodity cycle that included the pandemic contraction of 2020 and a period of significant global rate volatility. Mongolia is improving structurally, not just cyclically.

[Chart 1 above: Mongolia GDP per capita PPP 2018-2030, Source: IMF]

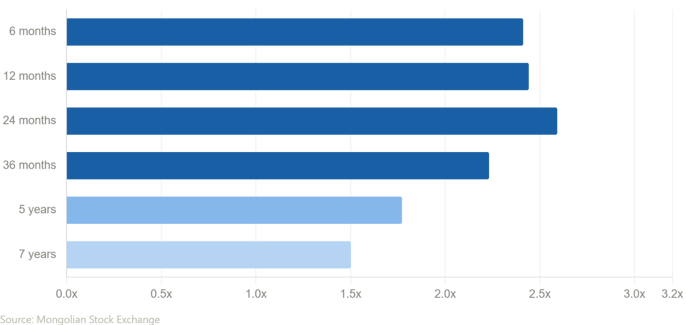

Mongolia’s rising wealth is reshaping domestic demand across asset classes. The domestic bond market offers one of the clearest signals of investor confidence. Government bond auctions have recorded bid-to-cover ratios of between 1.5 and 2.6 across tenors from six months to seven years, according to the Mongolian Stock Exchange. A bid-to-cover above 2.0 across short and medium tenors means domestic appetite for sovereign paper comfortably exceeds supply. That is not the picture of a market priced for distress.

[Chart 2 above: Domestic government bond bid-to-cover ratios by tenor, Source: Mongolian Stock Exchange]

The equity side is still developing, but the returns are becoming harder to ignore. The MSE-A index reached 19,796 in 2025, up from 9,532 in 2020. The MSE-B reached 15,197 over the same period, from 7,951. These are not liquid markets by developed-world standards, but the directional signal is consistent: domestic capital is being deployed and finding returns.

[Chart 3 above: MSE index performance 2020-2025, Source: Mongolian Stock Exchange]

Real estate is the most immediately accessible channel for international investors. NSO data shows investment in real estate activities reached US$52.2 million in 2024, up from US$17.7 million in 2022. Gross rental yields are estimated in the range of 8 to 11%, against a regional norm in major Asian cities of 3 to 5%. Price-to-rent ratios appear significantly lower than comparable Asian markets, according to Global Property Guide. The market has not yet found the capital that would normalise it.

The investment case for Mongolia in 2026 is not that the risks have disappeared. It is that the returns on offer relative to those risks have improved significantly, while many global investors still have not built the market into their coverage universe. That is unlikely to last. On the metrics that matter most — equities, domestic bonds, real estate yields, and income growth — the window for early-mover advantage is narrowing.