Frontier market investors will not find perfection but rather relative improvement. In recent years, that distinction has become increasingly important across Asia. Investors reassess political risk, supply chains, and long-term capital allocation. Mongolia is emerging as one of the beneficiaries of that reassessment.

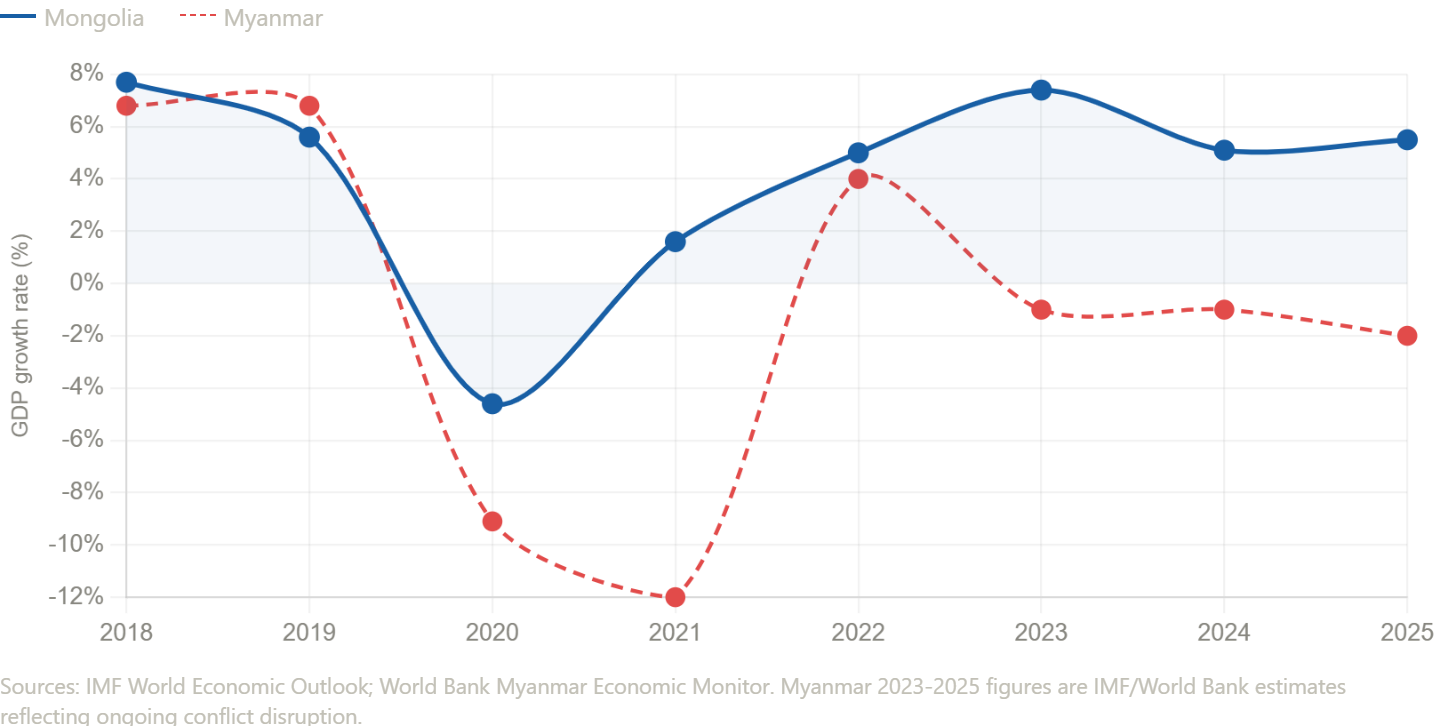

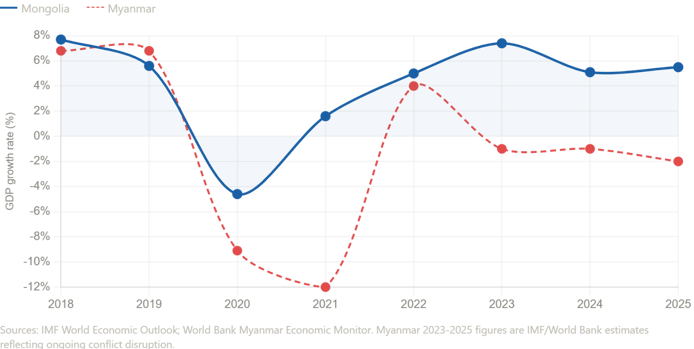

Myanmar once occupied a prominent place in frontier market discussions. Following economic reforms during the 2010s, international investors viewed the country as one of Southeast Asia’s most promising growth stories. Political instability and ongoing conflict have fundamentally altered that outlook. Many investors who previously allocated capital to Myanmar have been forced to reconsider frontier market exposure, elsewhere in Asia.

Mongolia vs Myanmar GDP growth 2018-2025. Myanmar: +6.8% (2018-19), -9.1% (2020), -12% (2021 coup), partial recovery then back into contraction. Mongolia: resilient through the same period

Mongolia presents a different proposition. The country remains a frontier market, but its investments increasingly rest on institutional improvement rather than political transition. Economic growth has remained resilient, supported by rising mineral exports, infrastructure development, and expanding participation in global supply chains. Copper, coal, and gold exports continue to generate substantial foreign exchange earnings while supporting government revenues and private investment.

The shift reflects broader changes in global capital markets. Since the pandemic, investors have become more focused on supply chain resilience and geopolitical diversification. Countries that can provide strategic resources, reliable export routes, and stable investment environments have attracted renewed interest. Mongolia’s role as a supplier of critical minerals aligns closely with these priorities.

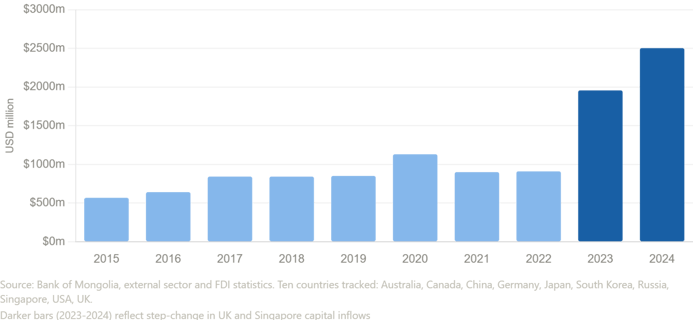

Total FDI inflows into Mongolia 2015-2024, showing the 2023-24 surge to $2.5bn from $568m in 2015

Geography also matters. While many global supply chains remain exposed to maritime chokepoints, including the Strait of Hormuz and major shipping corridors in the South China Sea, Mongolia’s export model is fundamentally land-based. This does not eliminate geopolitical risk, but it creates a different risk profile than resource exporters dependent on vulnerable maritime routes.

Infrastructure improvements have reinforced this advantage. Rail connections linking major mining regions to border crossings have increased export capacity and reduced transportation bottlenecks. Long-term resource exposure must consider logistics alongside geology. Mongolia’s progress on both fronts strengthened its competitive position.

The comparison with Myanmar does not suggest that Mongolia is risk-free. Frontier markets rarely are. The more relevant observation is that risk is being repriced across the region. Investors see where uncertainty is increasing and where it is more manageable.

Mongolia vs Kazakhstan vs Uzbekistan GDP growth 2018-2025, the Central Asian peer comparison

Mongolia’s growing importance in critical mineral supply chains, combined with improving infrastructure and stable economic growth, has positioned it favorably within the evolving frontier market landscape. The question for investors is which countries stand to benefit most from these reallocations.