Mongolia’s international bond market is no longer a one-name sovereign story. Last year, Mongolian issuers raised US$1.5 billion from international capital markets, a volume that would have been almost unthinkable a decade ago. For most of Mongolia’s modern financial history, international debt issuance meant the sovereign went to market and came back with money, while much else happened domestically in Tugrik. That structure worked for its time, but it was not much of a market.

2025 showed something more durable: Mongolia now has a broader, deeper, and more investable credit market.

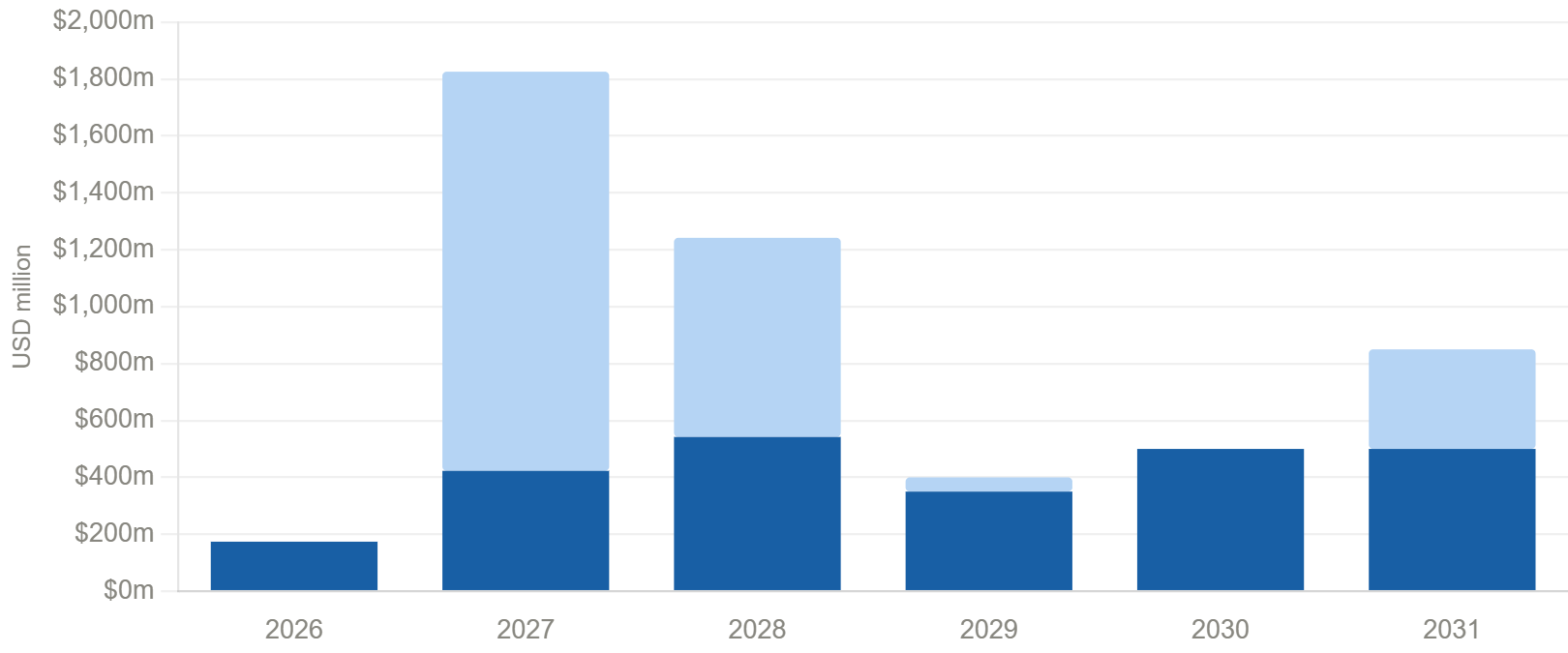

Sovereign

Quasi-sovereign / corporate

Source: Capital Markets Mongolia, repayment schedule as of January 2025

The sovereign set the tone early. The new five-year bond, issued in January 2025, priced at 222 basis points over US Treasuries, the tightest spread in Mongolia’s history according to Capital Markets Mongolia. The deal was oversubscribed 7.8 times. Spreads across the curve subsequently compressed, shorter-dated yields moved into the 5–6% range, and the 2028 and 2029 instruments moved above par. The message from institutional investors was clear: Mongolia’s credit has moved from watchlist curiosity to allocatable frontier exposure.

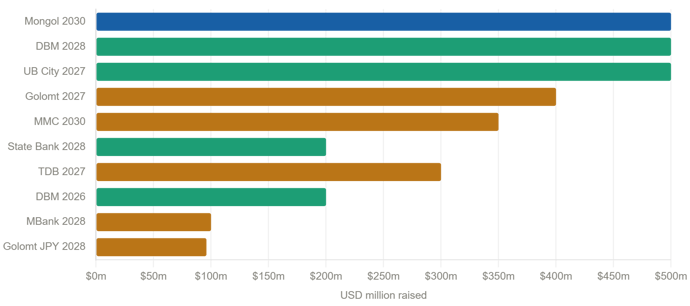

The more important development sits below the sovereign curve.

Sovereign

Quasi-sovereign

Corporate

Source: Capital Markets Mongolia / Bondblox · Note: Golomt JPY 2028 converted from JPY 15bn at approximate rate

The Development Bank of Mongolia returned to market with its 2028 bond, upsized from US$350 million to US$500 million on the back of investor demand. This was the largest private placement for a non-sovereign guaranteed credit in Mongolia, according to Capital Markets Mongolia. The City of Ulaanbaatar issued a US$500 million bond backed by a full sovereign guarantee, the first sovereign-guaranteed municipal bond in Asia. State Bank followed with a debut green bond, adding to the ESG-labelled supply that TDB and Golomt had begun building in prior years.

Then came the corporates. Golomt Bank completed a JPY 15 billion Samurai bond in the Japanese debt markets, the first such issuance by a Mongolian entity, guaranteed by Sumitomo Mitsui Banking Corporation. MBank, a smaller commercial bank without a parent affiliate guarantee, made its international debut independently. Mongolian Mining Corporation restructured its capital and issued callable notes. Yields across these corporate names have converged toward the 8–9% range, compressing from the double-digit levels that characterised the market only two years ago.

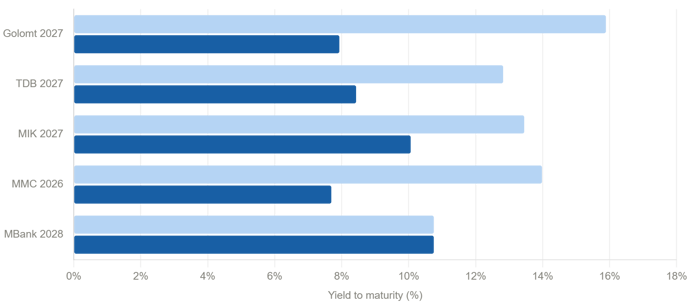

Historical high

2025 low

Source: Capital Markets Mongolia / Bondblox · Yield ranges from inception to October 2025

For a frontier market of Mongolia’s size, the number of distinct issuers accessing international capital in one year matters. Each completed transaction expands the investor base, creates another pricing point, and makes the asset class easier for allocators to understand. Tightening spreads also make Mongolia more legible to investors who might previously have dismissed it as too niche, too illiquid, or too difficult to model.

The repayment schedule is concentrated: US$1.83 billion falls due in 2027, followed by US$1.24 billion in 2028, according to the CMM outlook. The Mongolian parliament has approved up to US$1 billion in new sovereign issuance for 2026. This suggests the government is thinking about liability management, despite political uncertainty and commodity price volatility.

A market where the sovereign, a development bank, a municipal authority, a state commercial bank, a private bank, and a mining corporate can all access international capital in the same year is no longer dependent on a single point of failure. That is what bond market liquidity looks like in a frontier context.

Mongolia’s bond market story reaches a wider audience in Shanghai this month, where Capital Markets Mongolia presides over another Mongolia Investment Forum. For investors watching from Asia, the conclusion should be more direct: Mongolia is no longer just a sovereign refinancing story. It is becoming a layered credit market, and investors who wait for it to look fully mainstream may find that the spread compression has already happened.